Choosing between an FSA (Flexible Spending Account) and an HSA (Health Savings Account) can feel confusing. Both help you save money on medical costs, but they work differently.

People search for “fsa or hsa” because they want to know which account saves the most money, what rules apply, and how to use them effectively.

If you’re like most employees or self-employed individuals, understanding the differences can save hundreds, even thousands, of pounds or dollars each year.

This article breaks down the fsa or hsa question step by step. You’ll learn their definitions, origins, rules in the US vs UK, common mistakes, examples of usage, and which option might be best for you.

By the end, you’ll be confident when deciding between an FSA and an HSA and know exactly how to use them for maximum benefit.

FSA or HSA – Quick Answer

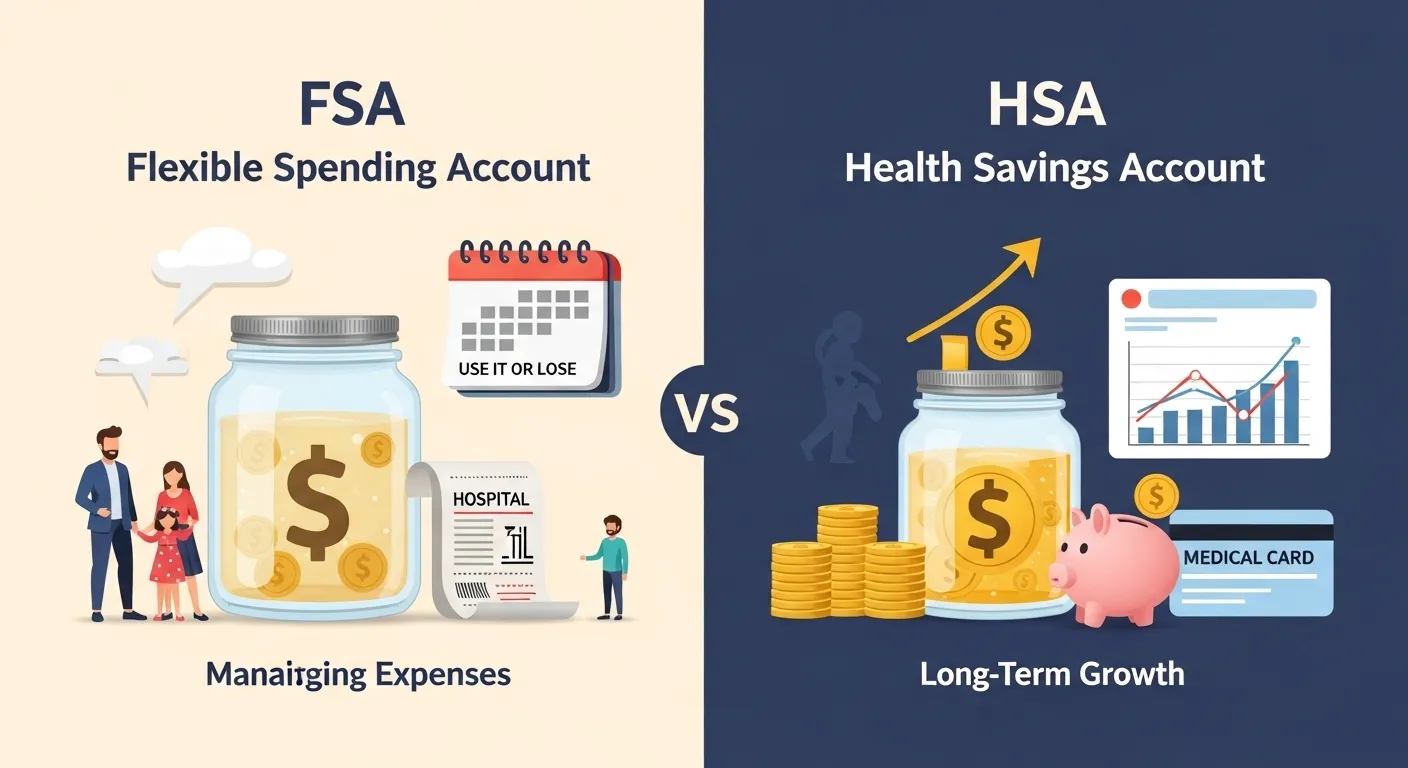

FSA (Flexible Spending Account) and HSA (Health Savings Account) are both accounts that let you save money on medical expenses using tax-advantaged funds.

- FSA: Offered by your employer. Money is contributed pre-tax, but you usually must spend it within the plan year. Unused funds may be lost.

- HSA: Available only with high-deductible health plans (HDHPs). Contributions are tax-deductible, money rolls over year to year, and funds can even be invested.

Example:

- You spend £200 on prescription glasses. With an FSA, that £200 comes from pre-tax dollars in your account. With an HSA, the same £200 also comes tax-free, but you could carry over any unused balance to the next year.

Quick takeaway: Use an FSA for predictable yearly expenses. Use an HSA for long-term savings and investment opportunities.

The Origin of FSA or HSA

- FSA: Introduced in the 1970s in the US as a way for employees to set aside money for medical costs before taxes.

- HSA: Introduced in 2003 as part of the Medicare Prescription Drug, Improvement, and Modernization Act. It was designed to give Americans a savings account they could grow over time for healthcare expenses.

The main reason people get confused is that both use tax-advantaged dollars for healthcare. FSAs are employer-based, while HSAs are tied to insurance plans. Their origins explain why their rules differ significantly.

British English vs American English Spelling

Interestingly, FSA and HSA are acronyms primarily used in American English. In the UK, you won’t find HSA often, but FSA exists for other purposes (like Food Standards Agency).

| Feature | US English | UK English |

| FSA | Flexible Spending Account | Rarely used for health; usually Food Standards Agency |

| HSA | Health Savings Account | Not common |

| Usage | Employee benefits, tax-advantaged medical savings | Mostly regulatory or agency names |

Key point: When writing for a UK audience, clarify what FSA or HSA means. Avoid assuming everyone knows the American healthcare context.

Read More Utmost or Upmost: Know the Correct Word and Usage Today

Which Spelling Should You Use?

- US audience: Use FSA or HSA as standard. These terms are widely recognized in employee benefits and insurance contexts.

- UK or Commonwealth audience: Use full explanations like “tax-free medical savings account” for clarity. Include FSA/HSA in brackets if needed.

- Global audience: Always explain abbreviations. Many readers may not be familiar with American healthcare systems.

Common Mistakes with FSA or HSA

- Mixing up eligibility: Only HSA requires a high-deductible health plan. FSAs are employer-dependent.

- Forgetting the “use it or lose it” rule: FSAs often expire at year-end; HSAs do not.

- Assuming both are interchangeable: HSA has investment benefits; FSA doesn’t.

- Over-contributing: Both accounts have annual limits set by the IRS (US) or employer policies.

- Not tracking receipts: IRS may require proof of qualified expenses.

Correction tip: Always check your plan documents and IRS guidelines for exact rules.

FSA or HSA in Everyday Examples

Emails:

“Hi John, I submitted my FSA reimbursement request for my eye exam last week.”

News:

“Americans are increasingly using HSAs to save for future healthcare costs amid rising insurance premiums.”

Social Media:

“Pro tip: Max out your HSA this year to save on taxes and build a healthcare nest egg!”

Formal Writing:

“Employees may elect to contribute to either an FSA or HSA, depending on eligibility and plan requirements.”

FSA or HSA – Google Trends & Usage Data

According to Google Trends, searches for “HSA” peak in January and February, aligning with new insurance plans and tax season. “FSA” peaks similarly but slightly lower overall.

Country popularity:

- United States: High

- Canada & UK: Very low, unless explaining American systems

- Global audience: Mostly interest from expatriates or finance/insurance professionals

This shows that “fsa or hsa” searches are primarily US-centric, confirming the need for context when writing for international audiences.

FSA vs HSA – Comparison Table

| Feature | FSA | HSA |

| Eligibility | Employer-based | Must have HDHP |

| Contribution Limits (2026) | $3,050 per year | $3,850 individual / $7,750 family |

| Tax Benefits | Pre-tax contributions | Tax-deductible contributions, tax-free growth, tax-free withdrawals for medical |

| Rollover | Usually use it or lose it | Money rolls over indefinitely |

| Investment | No | Yes, can invest in mutual funds, stocks, etc. |

| Best For | Predictable, short-term expenses | Long-term savings and investment |

FAQs About FSA or HSA

- Can I have both an FSA and HSA?

Usually not fully. Limited FSA options (like “limited-purpose FSA”) exist alongside HSA. - Do unused FSA funds roll over?

Some employers allow $610 to roll over (US 2026), but generally, it’s “use it or lose it.” - Are contributions tax-deductible?

Yes, both reduce taxable income, but HSA offers additional growth benefits. - Can I invest my FSA money?

No, only HSA funds can be invested. - Who owns the account?

FSA is employer-owned; HSA is owned by you. - Can I use HSA for non-medical expenses?

Yes, but it may incur taxes and penalties if under 65. - Do these accounts affect insurance premiums?

Not directly. HSA requires a high-deductible plan; FSA does not affect premiums.

Conclusion

Deciding between FSA or HSA depends on your health coverage, financial goals, and spending habits.

FSAs are great for short-term, predictable healthcare costs, but unused funds may be lost. HSAs are ideal for long-term savings and investment, offering unmatched flexibility and growth potential.

For US audiences, understanding contribution limits, eligibility rules, and tax advantages is key. For UK and global readers, provide context and explain acronyms clearly to avoid confusion.

Tracking expenses, staying within contribution limits, and planning for the year ahead ensures maximum benefit from either account.

Ultimately, both FSA and HSA can help you save money on healthcare, but choosing the right one requires knowing your options, plan type, and financial goals.

Plan carefully, contribute wisely, and watch your healthcare savings grow.

Claire Keegan an Irish author famous for powerful short stories. She writes in a clear and emotional style.